Get REC-ked

A Penny For Your Sins

In Medieval Europe, the Catholic Church granted indulgences to sinners as a Godly intercession to reduce punishment, both on earth and in the afterlife. Although these were originally intended to be service-oriented actions, such as prayer, pilgrimage, or caring for the church community’s old and poor, by the late Middle Ages, indulgences had degenerated into purely transactional agreements, where wealthy lawbreakers could purchase their way to freedom and salvation. This rot at the core of the Papacy provoked the Protestant Reformation, and the practice of selling indulgences was ultimately forbidden by Pope Pius V in 1567.

Now, almost 500 years later, it would seem what’s old is new again. Corporations today chase green-plated Environmental, Social and Government (ESG) scores, signaling to other virtue-signalers that they are ethical and responsible, and therefore desirable investments. One easy trick to gin up a high ESG credit rating is through buying Renewable Energy Certificates (RECs). According to the EPA, RECs are defined thus:

A renewable energy certificate, or REC (pronounced: rěk, like wreck), is a market-based instrument that represents the property rights to the environmental, social, and other non-power attributes of renewable electricity generation. RECs are issued when one megawatt-hour (MWh) of electricity is generated and delivered to the electricity grid from a renewable energy resource.

Oh Ye of Little Faith

When a wind or solar plant generates 1MWh of electricity, it is entitled to sell the carbon reduction benefits to a counter-party. Each individual REC can only be sold once, and then retired, in order to prevent accounting double-dipping. There are two main types of RECs: bundled and unbundled. Bundled RECs are sold with the environmental benefits attached to the underlying electricity generation, ensuring the purchaser actually uses the “clean” energy. Unbundled RECs sell only the environmental benefits of the initial power generation, and this is where the funny business starts. Corporate buyers of unbundled RECs are allowed to trade money for a certificate that can be used towards claims of reaching ESG goals such as “100% renewable” electricity sourcing, without a concomitant reduction in fossil fuels they use to manufacture and distribute goods and services (Scope 2 emissions). Sound familiar?

Because the renewable electricity has already been generated, and the unbundled REC has no effect on the actual emissions of the buyer, these types of financial instruments serve as little more than an opportunity to re-arrange deck chairs on the Titanic: they do nothing to reduce overall GHGs. Indeed, a study by Bjorn et al published in Nature in 2022 analyzed the RECs purchasing habits of 115 companies. The researchers found that while the companies had claimed an aggregate reduction of 30.7% in Scope 2 GHG emissions, unbundled RECs made up the majority of those fictitious reductions. Real emissions were only reduced by 9.9%.

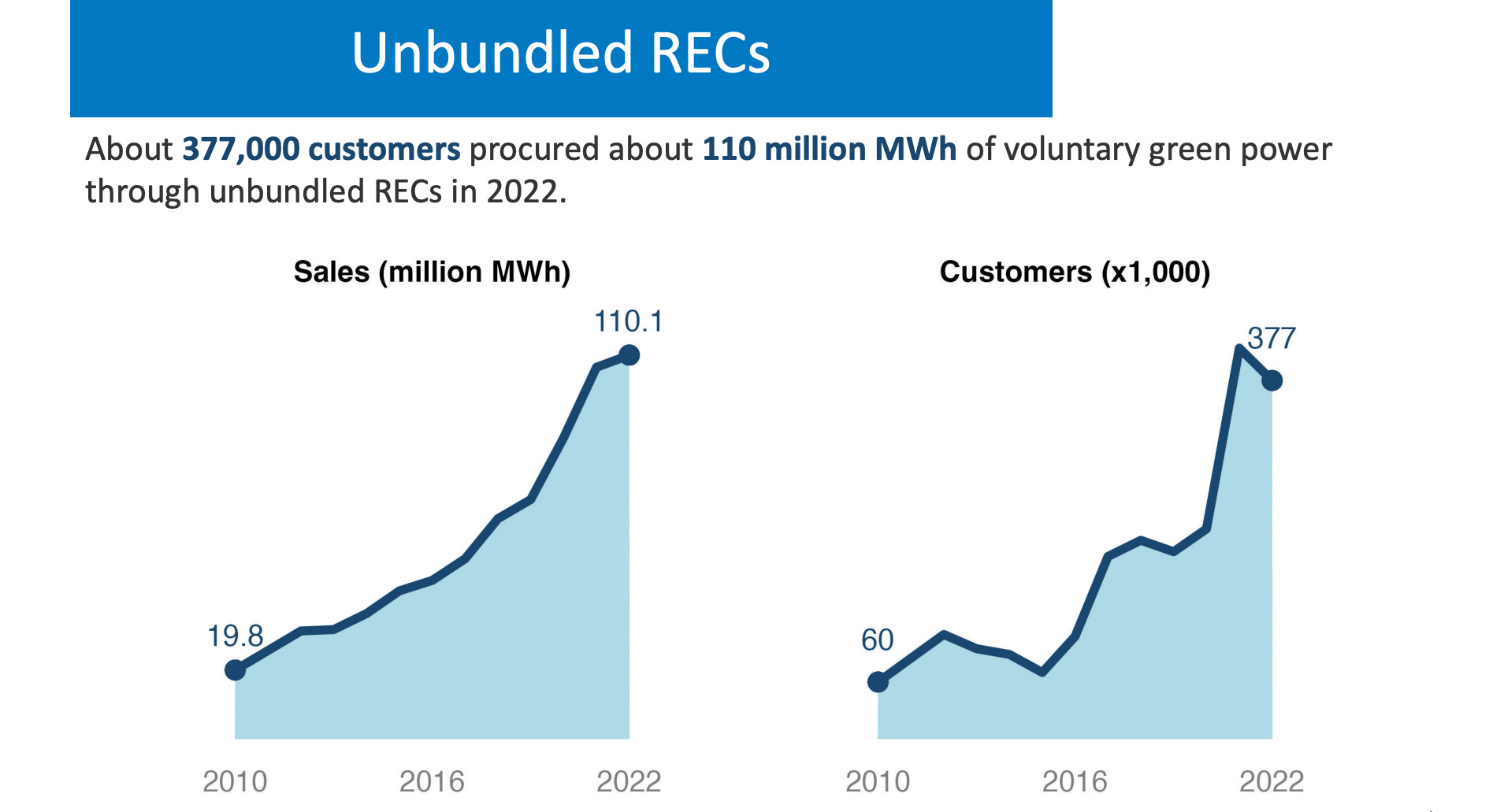

Even for the physics-illiterate corporate and government entities involved in the RECs sham, the path of least resistance is an iron law, and business is booming. The graphs below, from the National Renewable Energy Laboratory (NREL), show the increase in overall sales and corporate purchasers of unbundled RECs from 2010 to 2022 (the most recent report).

Moreover, unbundled voluntary RECs are relatively cheap, and they can be purchased across state lines. Unbundled RECs are generally oversupplied due to the low cost of entry into the market. The Carbon Offset Guide estimates that these RECs cost about $0.8-$2.00/MWh, depending on fluctuating wholesale generation and demand costs. For example, a solar plant in California supplying surplus energy to the grid during the middle of the day when electricity is at its cheapest can sell a REC to a fossil-fuel guzzling factory in Utah for about a buck. However, the value accrued to the buyer is much more than $1, because the purchase allows the company to cook its ESG books, which ultimately fetches attraction from high-roller institutional investors, and increases share prices. They also receive positive press and accolades from non-profit foundations and consumer watchdog groups, which can increase their customer base and profitability.

In a fascinating interview published by Reveal, journalist Will Evans discussed the economics of RECs with Auden Schendler, CEO of Aspen Skiing Company, who had a change of heart after realizing the duplicitous fraud involved in purchasing the certificates. Schendler disclosed that for $42,000 (a tiny portion of the company’s energy budget), he bought 20,000 RECs, and with them, the bragging rights to claim that the ski lodge had offset 100% of its electricity with renewable energy resources (while doing nothing to change the actual fuel usage onsite).

Dazed and Confused

Another problem with the RECs market is its dependence on convoluted reporting processes for underlying assets to get credit for their generating capacity. At the same time, poor oversight may also allow solar and wind farms to get away with exaggerated productivity claims. This problem is especially acute in states designated as compliance markets, where the state legislature mandates a certain percentage of electricity to be sourced by wind and solar, and utilities and suppliers can be held civilly liable for noncompliance.

In California, all load-serving utilities are required to submit reports certifying that their generation stations meet the Renewables Portfolio Standard. However, recently there has been a significant backlog in utility ability to track RECs, due to software malfunctions in the Western Renewable Energy Generation Information System (WREGIS), which verifies all transactions associated with RECs across 14 western states.

This issue came up for discussion as an agenda item at the business meeting of the California Energy Commission on May 8. Per the meeting transcript, spokespersons from across the Investor Owned Utilities (IOUs), municipal utilities, and Community Choice Aggregators (CCAs) commented that the system was not properly logging and transferring RECs to the appropriate party. Josh Harmon from Pacific Gas and Electric (PG&E) said that the backlog, going back almost a year, affected 1.5 million RECs for PG&E. He also stated that “despite ongoing engagement with WREGIS there’s still a lack of transparency regarding outstanding issues and no clear timeline for resolution.”

If a software glitch can so easily disrupt and obfuscate who is really selling and buying verifiable RECs, it calls into question the integrity of the whole certification program. It is a market set up to be plundered by bad actors.

Shifting the Goal Posts

In recognition of the shortcomings of RECs, some companies have begun opting for Power Purchasing Agreements (PPAs), in which a renewables developer builds and operates generation systems on a customer’s property. This arrangement ensures that the onsite electricity at an industrial facility is at least partially supplied by zero emissions energy. However, because PPAs require intensive upfront capital to initiate, they are relatively limited to large corporations with deep pockets. Indeed, according to a Bloomberg study, over half of PPAs signed in 2021 were among big tech giants, such as Amazon, Microsoft, Meta and Google.

Recent policy changes are also likely to influence corporate behavior around the purchase of RECs and PPAs. In March 2024, the Securities Exchange Commission (SEC) adopted a new set of rules for emissions disclosures, applying to public companies designated as large accelerated filers (public float of $700 million or more). The SEC now requires large companies to disclose their Scope 1 and 2 GHG emissions on official filings, beginning fiscal year 2025. While the goal of such policy is ostensibly transparency for investors who seek to reward good corporate stewardship of environmental resources, it also creates a perverse incentive for companies to use underhanded methods of appearing more “green” than they actually are. It would not be surprising to see an uptick in unbundled RECs purchases or the development of new funny-money arrangements in the near future.

If there’s one thing consistent about human nature, it’s that any loophole opened by bad policy will ultimately be exploited. And as for any hope of salvation for indulgence buyers, medieval or modern, it would be easier for a camel to go through the eye of a needle.

Electrically yours,

K.T.

Thanks. I have been dubious about RECs and you clearly explained how they are of little value.

And not one bit of any of this reduces GHGs, but it does make many manipulators quite wealthy.

When Cap and Trade was introduced a dozen or so years ago, I was amazed at how many people thought it good policy. All one had to do was ask, "How does paying a tax to the state, reduce emissions?"

I am fully on board with the idea that all of this climate manipulation, is just as much of a scam to milk money into the accounts of the wealthy as is Covid, Ukraine, Obamacare, and many more.